SpaceX’s FCC filing for next-generation satellite deployment — combined with Elon Musk’s public disclosure of orbital data center specifications — has moved this conversation from science fiction to capital allocation decision. Three analysts weigh in on what it actually means.

Let’s start with what the FCC filing actually tells us, because the surface narrative — “SpaceX builds data centers in space, isn’t that cool” — is missing the structural point entirely.

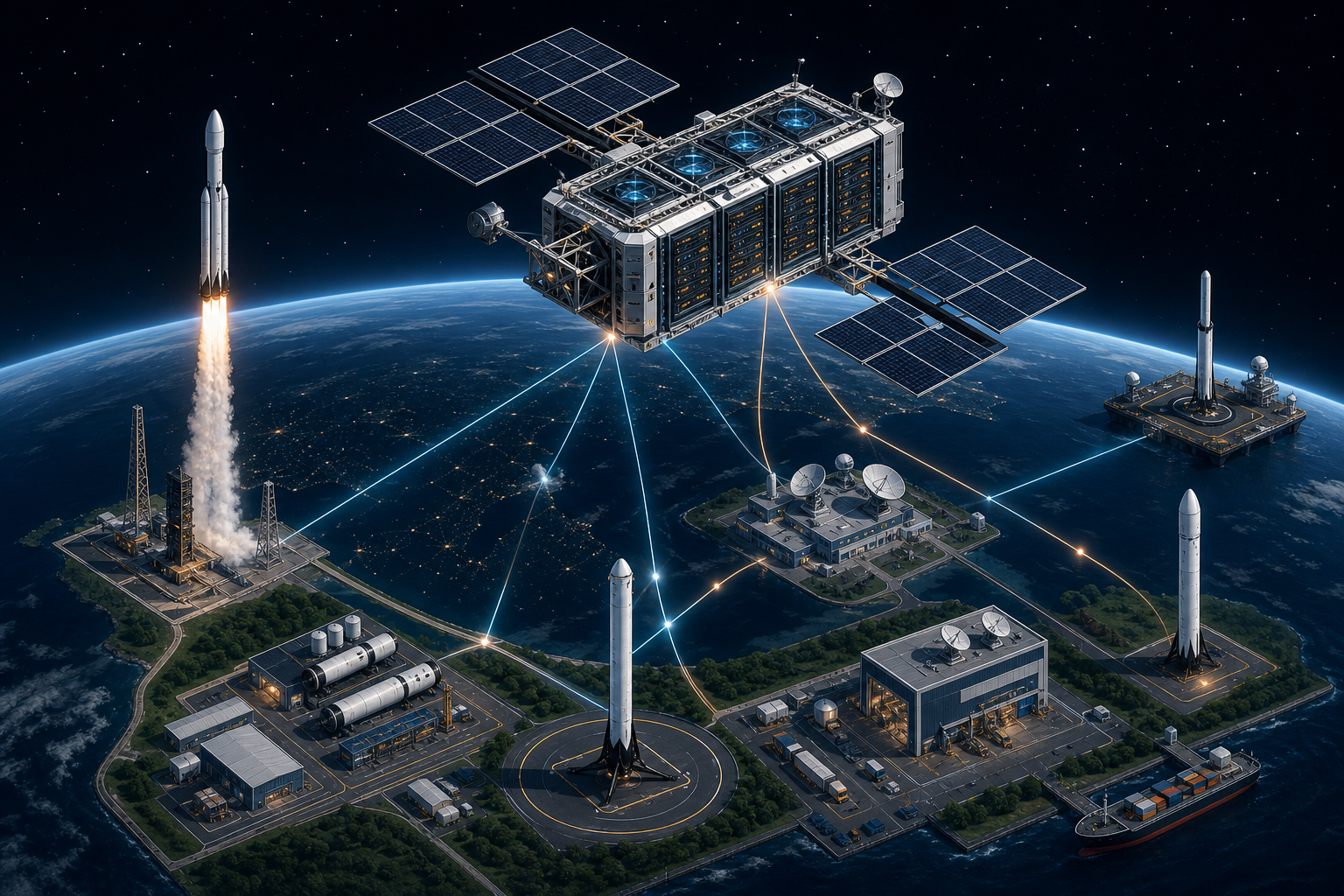

The satellite architecture Musk disclosed is dominated by two physical components: solar panels generating power, and 110-square-meter liquid radiator panels deployed vertically to dissipate heat. Nobody is talking about what that thermal management specification implies. On Earth, data center cooling is solved by geography — you locate near cold water, cold air, cheap grid power. In orbit, you have none of those options. You are engineering around a fundamental thermodynamic constraint that terrestrial operators never face. The radiator panel size alone tells you this is not a marginal efficiency play. This is a completely different cost structure, and the market is pricing it like it’s just a slightly more ambitious hyperscaler build.

Here is the institutional flow mechanic that concerns me. SpaceX raised $75 billion in its IPO with $250 billion in stated demand — retail participation was 56% of individual investor volume on day one, $117.6 million in retail flows in a single session. Eleven leveraged ETFs launched within the first week. That is a distribution structure built for momentum, not for the decade-long capital cycle this orbital infrastructure actually requires. The xAI Colossus build in Memphis — 100,000 H100 GPUs in 122 days — was impressive execution. But xAI is losing approximately $10 billion per quarter, and SpaceX moved to raise an additional $20 billion in corporate bonds within ten days of the IPO close. When a company raises $75 billion and immediately signals it needs $20 billion more, the question isn’t whether the technology works. The question is who bears the capital risk during the construction phase, and whether the current holder base — dominated by retail momentum — is positioned for that holding period. My strong suspicion: they are not.

The investor implication is concrete. The orbital data center story is real infrastructure ambition. The current capital structure is not matched to it. Watch credit spreads on the corporate bond issuance. If investment-grade ratings from Moody’s (Baa1), Fitch, and S&P hold through the bond raise, the institutional base may stabilize. If spreads widen materially, the retail leverage ETF layer unwinds fast. Korean institutional investors — already receiving only partial IPO allocations due to FX intervention concerns on a ₩7.5 trillion equivalent position — should be watching the bond market, not the stock price.

I’ll grant the technology is genuine. The bull thesis writes itself: proprietary launch infrastructure via Falcon 9 and Starship, vertical integration from rocket manufacturing to satellite deployment to orbital compute, and a regulatory moat that any competitor would need a decade to replicate. Starlink already demonstrates the business model works at scale — aviation contracts with Korean Air and others, 94%-load-factor carriers like Ryanair now negotiating connectivity deals. The infrastructure flywheel is real.

Now the risks, because they are substantial and the market is not pricing them adequately. First, the thermal physics problem the Macro Bear raised is also a unit economics problem. A 110-square-meter radiator panel per satellite is not a footnote — it is the dominant cost driver of the orbital form factor. Ground-based cooling for hyperscale data centers runs roughly $2-4 per watt of IT load in well-sited facilities. The orbital equivalent has no published comparable, which means analysts are extrapolating terrestrial economics into a fundamentally different cost regime. That is how you get valuation errors.

Second, map where we are in the infrastructure investment cycle. Dell’s ISG segment — which serves neo-cloud operators, enterprises, and governments, not hyperscalers — is showing explosive sequential revenue growth, traditional server demand is recovering alongside AI server demand, and DRAM prices have moved dramatically upward. This tells me terrestrial AI infrastructure demand is nowhere near saturation. The bottleneck sequence has been chips → advanced packaging (still the most acute constraint per current analysis of the 2025-2027 packaging investment map) → power. US data center power demand goes from 167 TWh in 2023 to a projected 376 TWh by 2030. We have not resolved the terrestrial power bottleneck. We are being asked to price orbital infrastructure before the ground-based version has cleared its own capacity constraints. That sequencing risk is underappreciated.

Third, governance. Moody’s flagged it explicitly alongside the Baa1 rating — the concentration of decision-making authority is a structural concern. Starbase, Texas was incorporated as a formal city in May 2025, governed substantially by SpaceX employees and their families, operating under exceptional autonomy granted by the Texas state government. Musk’s stated model — AI and engineers replacing elected officials in a “Mars technocracy” — is an ideological project, not just a business one. When ideology and capital allocation compete for the same balance sheet, value investors have historically lost.

Drill one layer below the space data center narrative and you find the real signal: this is a liquidity and capital structure story wearing a technology costume.

SpaceX raised $75 billion. Within ten days, it filed to raise $20 billion in corporate bonds. The stock dropped 16% on that announcement. The consensus read is “SpaceX needs money for xAI.” That is correct but incomplete. The mechanism matters. xAI’s cash burn — approximately $10 billion per quarter — is being socialized onto SpaceX’s balance sheet through the corporate structure. The IPO retail investor bought SpaceX. They got xAI’s burn rate as a liability. The question is not whether orbital data centers are viable in 2035. The question is whether xAI achieves positive unit economics before the capital markets lose patience. OpenAI and Anthropic both have stronger current market positioning. xAI is third, spending like first.

The international benchmark that Korean investors should be running: compare this to the floating data center parallel. Japanese shipping companies — Mitsui OSK Lines specifically — are converting car carriers into sea-based data centers, exploiting marine cooling and avoiding land acquisition costs. Samsung Heavy Industries is pursuing similar positioning. The economics are different but the structural logic is identical to the orbital play: go where conventional real estate and power grid constraints don’t apply. The difference is that a converted car carrier has a known construction cost, a defined cooling capacity, and operates in a regulatory environment with fifty years of precedent. The orbital equivalent has none of those anchors.

I hold the uncertainty openly here, which the current market is not doing. The power bottleneck is real — FERC is already compelling PJM, CAISO, and NYISO to review large-load interconnection rules within 60 days, and grid constraint is structural, not cyclical. If orbital solar-powered compute genuinely sidesteps terrestrial grid dependency, the TAM expands dramatically. But “if” is doing enormous work in that sentence. Battery storage scaling, advanced packaging availability, and grid reform are all proceeding on Earth in parallel. The probability that orbital infrastructure becomes cost-competitive before terrestrial solutions catch up is not high — it’s just not zero, which is what current sentiment implies. The Mirae Asset situation — returning the bulk of a ₩7.5 trillion allocation due to FX intervention pressure — tells you everything about the structural friction Korean capital faces in accessing this trade even if the thesis is correct.

Three analysts, one convergent conclusion dressed differently: the SpaceX orbital infrastructure thesis is technically credible, structurally premature, and currently mis-owned. The thermal physics are real. The capital burn is real. The retail leverage layer is fragile. The terrestrial infrastructure bottleneck — power, packaging, cooling — has not cleared, which means the market is pricing the orbital solution before the ground-based problem is fully monetized. Korean institutional investors face an additional structural constraint: FX intervention mechanics mean the most aggressive allocators are already capacity-limited. Watch the corporate bond spreads, not the stock ticker, for the first honest signal about whether this capital structure survives the construction cycle.